Featured

Table of Contents

- – Who offers Level Term Life Insurance Policy Op...

- – What should I look for in a Level Term Life In...

- – No Medical Exam Level Term Life Insurance

- – What should I know before getting Level Premi...

- – Why is Level Term Life Insurance Protection ...

- – Is Level Term Life Insurance Protection wort...

- – Level Term Life Insurance Policy Options

The primary differences between a term life insurance policy plan and a permanent insurance coverage (such as entire life or global life insurance policy) are the period of the policy, the buildup of a cash worth, and the expense. The right choice for you will depend upon your demands. Below are some points to consider.

People that possess entire life insurance policy pay more in premiums for much less protection however have the protection of understanding they are shielded forever. Level term life insurance coverage. Individuals who purchase term life pay premiums for an extended duration, but they get absolutely nothing in return unless they have the bad luck to die prior to the term expires

The performance of irreversible insurance can be constant and it is tax-advantaged, offering added benefits when the stock market is unpredictable. There is no one-size-fits-all solution to the term versus irreversible insurance coverage discussion.

The motorcyclist guarantees the right to convert an in-force term policyor one ready to expireto a permanent plan without going via underwriting or verifying insurability. The conversion cyclist should enable you to convert to any type of irreversible policy the insurance provider supplies with no constraints. The primary features of the motorcyclist are preserving the initial health and wellness rating of the term plan upon conversion (also if you later on have wellness problems or come to be uninsurable) and determining when and exactly how much of the protection to convert.

Who offers Level Term Life Insurance Policy Options?

Obviously, overall premiums will certainly raise significantly because entire life insurance is much more pricey than term life insurance coverage. The advantage is the ensured approval without a medical examination. Clinical conditions that establish during the term life duration can not create costs to be raised. The firm might require restricted or complete underwriting if you desire to include extra motorcyclists to the new plan, such as a long-term treatment rider.

Term life insurance policy is a reasonably affordable means to give a round figure to your dependents if something occurs to you. If you are young and healthy and balanced, and you support a household, it can be an excellent alternative. Entire life insurance policy includes substantially higher month-to-month premiums. It is implied to supply insurance coverage for as long as you live.

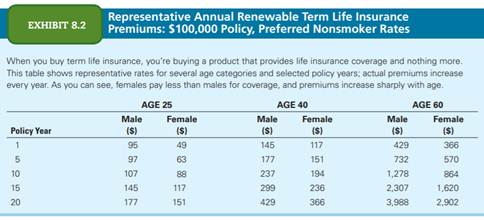

It depends upon their age. Insurance provider established an optimum age restriction for term life insurance coverage policies. This is normally 80 to 90 years of ages, however may be greater or lower depending on the firm. The costs additionally climbs with age, so an individual aged 60 or 70 will certainly pay significantly greater than someone decades younger.

Term life is somewhat comparable to automobile insurance policy. It's statistically unlikely that you'll need it, and the costs are money away if you don't. If the worst occurs, your household will get the benefits.

What should I look for in a Level Term Life Insurance Coverage plan?

A degree costs term life insurance policy strategy lets you stay with your spending plan while you assist shield your household. Unlike some tipped price plans that boosts yearly with your age, this type of term strategy offers rates that remain the exact same for the period you select, also as you age or your health modifications.

Find out more regarding the Life Insurance choices readily available to you as an AICPA member. ___ Aon Insurance Solutions is the brand name for the brokerage and program administration operations of Fondness Insurance policy Services, Inc. (TX 13695) (AR 100106022); in CA & MN, AIS Affinity Insurance Coverage Firm, Inc. (CA 0795465); in OK, AIS Affinity Insurance Coverage Services Inc.; in CA, Aon Affinity Insurance Coverage Providers, Inc.

No Medical Exam Level Term Life Insurance

The Plan Representative of the AICPA Insurance Policy Trust Fund, Aon Insurance Services, is not associated with Prudential. Team Insurance policy protection is provided by The Prudential Insurance Company of America, a Prudential Financial firm, Newark, NJ. 1043476-00002-00.

Essentially, there are 2 kinds of life insurance prepares - either term or permanent plans or some combination of both. Life insurance providers offer different types of term plans and standard life plans along with "interest sensitive" items which have become extra widespread given that the 1980's.

Term insurance provides protection for a specific amount of time - Level term life insurance vs whole life. This period can be as brief as one year or give insurance coverage for a specific variety of years such as 5, 10, twenty years or to a specified age such as 80 or in many cases as much as the earliest age in the life insurance policy mortality

What should I know before getting Level Premium Term Life Insurance?

Currently term insurance rates are extremely affordable and amongst the cheapest historically skilled. It must be noted that it is an extensively held idea that term insurance policy is the least pricey pure life insurance protection available. One needs to review the plan terms thoroughly to choose which term life options appropriate to fulfill your specific situations.

With each brand-new term the costs is boosted. The right to restore the policy without evidence of insurability is an important benefit to you. Otherwise, the danger you take is that your wellness might weaken and you may be not able to obtain a policy at the exact same rates or even in all, leaving you and your recipients without protection.

You must exercise this option throughout the conversion duration. The size of the conversion duration will certainly differ depending on the kind of term plan bought. If you convert within the proposed duration, you are not required to provide any kind of information about your health and wellness. The premium price you pay on conversion is generally based upon your "existing obtained age", which is your age on the conversion date.

Why is Level Term Life Insurance Protection important?

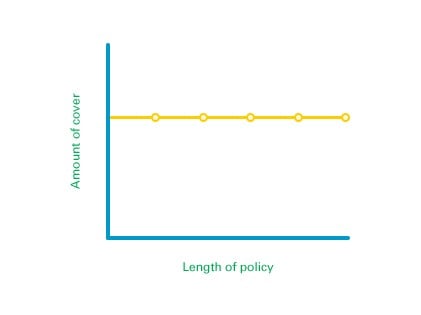

Under a degree term policy the face quantity of the policy continues to be the same for the entire duration. With decreasing term the face quantity lowers over the duration. The premium stays the same each year. Typically such policies are sold as mortgage defense with the quantity of insurance policy lowering as the balance of the mortgage reduces.

Traditionally, insurers have actually not can transform premiums after the policy is marketed. Given that such plans might proceed for numerous years, insurance providers should use conservative mortality, rate of interest and expenditure rate price quotes in the costs estimation. Flexible premium insurance coverage, however, permits insurance companies to use insurance policy at lower "current" costs based upon much less conventional presumptions with the right to change these costs in the future.

While term insurance coverage is made to supply protection for a specified period, permanent insurance coverage is made to supply insurance coverage for your whole lifetime. To keep the premium rate level, the premium at the younger ages exceeds the actual cost of security. This extra costs constructs a book (cash value) which assists pay for the plan in later years as the price of security increases over the costs.

Is Level Term Life Insurance Protection worth it?

With degree term insurance, the cost of the insurance coverage will remain the very same (or potentially reduce if dividends are paid) over the term of your plan, typically 10 or twenty years. Unlike long-term life insurance policy, which never runs out as lengthy as you pay costs, a degree term life insurance policy policy will end at some point in the future, commonly at the end of the duration of your degree term.

Since of this, several people make use of long-term insurance coverage as a stable financial preparation device that can offer numerous needs. You might have the ability to convert some, or all, of your term insurance policy during a collection period, commonly the first one decade of your plan, without requiring to re-qualify for protection even if your health and wellness has actually transformed.

Level Term Life Insurance Policy Options

As it does, you might wish to include in your insurance policy coverage in the future. When you first obtain insurance coverage, you might have little financial savings and a large mortgage. Ultimately, your financial savings will certainly expand and your home mortgage will certainly shrink. As this occurs, you may intend to at some point lower your fatality benefit or consider transforming your term insurance coverage to an irreversible plan.

Long as you pay your premiums, you can relax very easy recognizing that your loved ones will get a death benefit if you die throughout the term. Several term plans permit you the capacity to convert to long-term insurance coverage without needing to take another health and wellness exam. This can enable you to take benefit of the extra benefits of an irreversible policy.

{kind=link}

Table of Contents

- – Who offers Level Term Life Insurance Policy Op...

- – What should I look for in a Level Term Life In...

- – No Medical Exam Level Term Life Insurance

- – What should I know before getting Level Premi...

- – Why is Level Term Life Insurance Protection ...

- – Is Level Term Life Insurance Protection wort...

- – Level Term Life Insurance Policy Options

Latest Posts

What is the Function of Life Insurance Level Term?

How much does Wealth Transfer Plans cost?

How long does Low Cost Level Term Life Insurance coverage last?

More

Latest Posts

What is the Function of Life Insurance Level Term?

How much does Wealth Transfer Plans cost?

How long does Low Cost Level Term Life Insurance coverage last?